But worth it…

Funny thing, this financial planning stuff. You are asked to guess, for the coming years or even decades, how much will you be spending every year, and how much income or growth will your money deliver, and also, when will you die!

If we knew all of this with certainty, there isn’t much left to life itself! Some people plan their expenses so meticulously to deplete their savings so they can die with almost nothing to their name, while some may even max out the credit cards knowing it is their last month on the planet!

As long as we are dealing with assumptions, let’s address one that people often under-estimate. This assumption especially impacts people who are planning to retire early on relatively modest spending budgets.

I am referring to the assumption of not earning even a penny during retirement. If you are looking at a 40 year horizon, that’s 14,600 days, or 350,400 hours! An enormous amount of time that an early retiree who has earned back – their ‘personal time’ to do as they please. With all this time available for pursuing our interests, even our hobbies can turn into income-generators. It doesn’t matter what that income is, but if you are spending budget is relatively modest (under $50,000 a year), then even a small bit of income will matter immensely to your retirement planning success or to your peace of mind!

For this article, I will start off with the most conservative financial planning scenario I analyzed in my previous post: Hacking The Retirement Calculators. Reading that article first may be a useful primer for this post. Anyway, in that post, we were interested in finding the safest withdrawal rate, using the boundary condition of a ‘failure edge’ under the widest possible swing in portfolio values (this is achieved by 100% stock allocation).

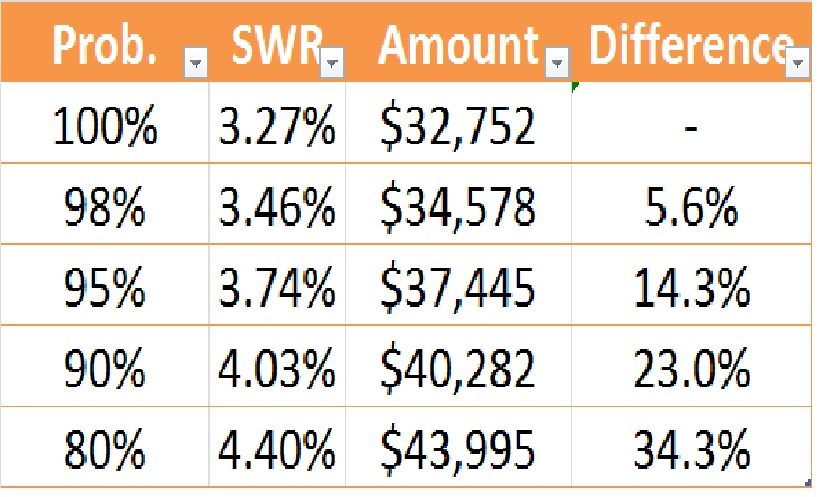

We found that the safest withdrawal rate is 3.27% for a 50-year retirement horizon at a 100% success rate (can’t go any higher!). We did this exercise for a $1 million portfolio, efficiently invested in stock index funds at a low 0.1% overall expense ratio. This scenario considers zero income or pension or social security benefits over the entire 50-year horizon. We then relaxed the success rates till 80%. In doing this, I considered that success rates beyond 80% is ‘vanity’ as the good doctor – and author of The Four Pillars of Investing: Lessons for Building a Winning Portfolio – Dr. William Bernstein says. The goal was to see how this increases the withdrawal rates compared to the safest scenario of 100% success rate. That table is here:

SWR changes with your required probability of success

Notice how much your withdrawal amounts increase when you relax the success rate even slightly. A modest relaxation to 95% success rate, which in practical terms is as certain as you will be alive tomorrow, allows the withdrawal to increase by 14%. That’s a big jump. Imagine what you could do with an additional nearly $3000 to spend each year? That pays for a nice European vacation – every year – for a retired couple!

But what if you are a scared-y cat? What about people who demand – however meaningless it may be in terms of real life – as close to a full certainty in financial success? What if you cannot tolerate even a 5% chance of having to spend below your budgeted amount. That’s right. A 5% chance of failure in the above table doesn’t mean you are out on the streets! It means that your spending level may have to be cut down during difficult times so that your portfolio can survive the rare 1 in 20 case of a multi-decade poor economy and markets. This still means that in 19 out of 20 cases, you will not only be fine but will have a higher ability to spend than the $37,445 figure mentioned.

But what if you are a scared-y cat? What about people who demand – however meaningless it may be in terms of real life – as close to a full certainty in financial success? What if you cannot tolerate even a 5% chance of having to spend below your budgeted amount. That’s right. A 5% chance of failure in the above table doesn’t mean you are out on the streets! It means that your spending level may have to be cut down during difficult times so that your portfolio can survive the rare 1 in 20 case of a multi-decade poor economy and markets. This still means that in 19 out of 20 cases, you will not only be fine but will have a higher ability to spend than the $37,445 figure mentioned.

Yeah, but I still cannot tolerate even a 5% risk, you say? Well, this is where the tiny income super charges a modest spending budget!

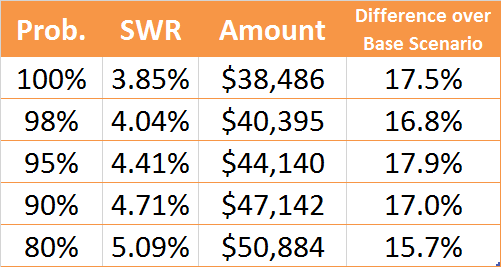

In the same scenario above, let’s assume you convert your hobby into a partial income of say $1000 a month and you keep this hobby up for half your retirement horizon (that is, 25 out of 50 years). Let’s also assume this figure doesn’t change with inflation, so it remains the same $1000 in the first year and even in the 25th year of your retirement! I made this assumption to compensate for the declining hours you may spend in the future for the same hobby so even if the ‘per hour’ value increases in inflation, you may be spending less hours as you age pursuing your hobby. For the same 50 year scenario, we get these results in cFIREsim.

The benefit of a casual hobby income extends far beyond your life satisfaction!

For the same 100% ‘safest’ case, you can now withdraw 17.5% more than in the base case above, that is, nearly $5000 more every year! Are you wondering, why does a $1000/month income ($12000 per year) result in only about $5000 more in spending? Shouldn’t it add up directly to the previous table’s SWR? The answer lies in inflation adjustment, as in, we didn’t do any! It also lies in the fact that we assumed that this income only lasts for the first half of your 50-year retirement. Still, this shows us how much of a better life our portfolio allows us to spend – with the same warm and fuzzy assurance of 100% success rate – if we had a modest hobby income on the side.

What if you don’t want to do that? Well, we will consider a case where instead of a hobby income, we will allow for a modest social security or pension to kick-in at a later age.

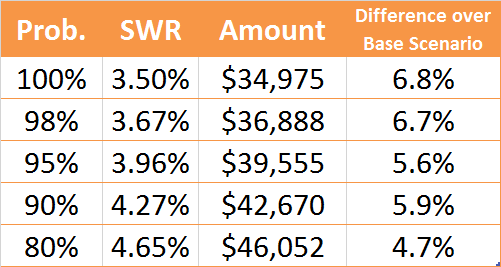

For the next case, we assume you don’t earn even a single penny from any hobby. But you have a tiny social security or equivalent pension that kicks in age 67, whose present value is $10,000 per year or $833.33 per month. The reason I assumed a low figure here is that an early retiree at age 45 – though vested in the system – will not have contributed much to get the maximum possible benefit. Moreover, the average social security figures are hovering around $16,000 per year, which I deduct 25% (based on projections of depleting social security trust fund) to get $12,000 per year. I further take a 20% haircut on this figure to be conservative to provide for any future statutory deductions or taxes, and consider only $10,000 per year in social security (or your country’s equivalent pension) to flow in from age 67. One key difference here compared to previous case is that this figure is inflation-adjusted, and normally bench-marked to consumer price index. But this only starts at age 67, so for a 45-year old early retiree, this modest pension is 22 years away. With all other factors remaining the same as the previous case, we get this table after the modeling this change:

Every little bit matters.

The differences over base case here are not as significant. That’s because of the low pension/social security figure we assumed deliberately for this analysis, and also, this doesn’t show up for the first 22 years of the 50-year retirement period. Moreover, the success probabilities are driven more by withdrawal rates in early years – in this case, there’s any contribution for the first 22 years. Still, there is a meaningful increase in withdrawal amounts for each of the success probabilities assumed. A large part of ‘safe’ withdrawal depends on the first 10 years of your retired life. If you cross that with your portfolio intact, then you are good to go for the rest of your life.

Takeaways

You have a choice to make if you want 100% certainty!

The main takeaway is that even a tiny income – either in the first half or latter half of your retirement time frame – makes a meaningful difference to your success. This is obvious, right? What may not be so obvious is that people – who demand or are comforted only by – 100% probability of success in these simulations are better off generating some income (no matter how small) during the first one or two decades of their early retirement. The choice is yours – take the blue pill or the red pill! Either earn some side income now or be assured about the solvency of your country’s old age pension program!

Raman Venkatesh is the founder of Ten Factorial Rocks. Raman is a ‘Gen X’ corporate executive in his mid 40’s. In addition to having a Ph.D. in engineering, he has worked in almost all continents of the world. Ten Factorial Rocks (TFR) was created to chronicle his journey towards retirement while sharing his views on the absurdities and pitfalls along the way. The name was taken from the mathematical function 10! (ten factorial) which is equal to 10 x 9 x 8 x 7 x 6 x 5 x 4 x 3 x 2 x 1 = 3,628,800.

6 comments on “The Value of a Tiny Income”