We spend a lot of effort chasing our number or desired passive income to reach our financially independent or retired early (FIRE) dream. In all the search for ‘how much’, we also need to consider ‘how long’. With some retiring in early 30’s, the impact of this extreme early retirement should be carefully considered. If you are like me in 40’s or even in 50’s, there is at least one advantage we have over our 30’s retired brethren – our retirement planning is not as long. Don’t let that depress you. It’s the life you add to the years, not the years you add to life that matters! As Yoda would say: matter it doesn’t!

We spend a lot of effort chasing our number or desired passive income to reach our financially independent or retired early (FIRE) dream. In all the search for ‘how much’, we also need to consider ‘how long’. With some retiring in early 30’s, the impact of this extreme early retirement should be carefully considered. If you are like me in 40’s or even in 50’s, there is at least one advantage we have over our 30’s retired brethren – our retirement planning is not as long. Don’t let that depress you. It’s the life you add to the years, not the years you add to life that matters! As Yoda would say: matter it doesn’t!

For the purpose of this article, I will use illustrative examples of Adam, Betty and Charlie, three happily retired people, and they all retired early compared to the ‘official’ retirement age (of 60-70, depending on who you ask). All three of them have the following in common:

- Just retired this year

- All have similar tax profiles, so we ignore taxes and social security for the purpose of analysis

- All are single with no dependents, no inheritance and no pension.

- Have $1 million in investment portfolio for retirement – that’s the only thing they have to depend on.

- Equal tolerance for volatility and they invest efficiently – 100% in US total stock market index fund or ETF charging just 0.1% in fees

- Because the portfolio is always 100% stock, there is no need for re-balancing.

- Plan to live till 90

- All are equally frugal (or too spendy, as Jacob might see it), requiring $40,000 a year to live on (2016 dollars, inflation adjusted) with future spending pegged to inflation.

What’s the difference between them? Age. Adam is 35, Betty is 45 and Charlie is 55. Thus, the only difference between the three early retirees is the retirement span (or length).

For generating the data for this article, I used FIRECalc, though you can use any retirement calculator with accurate historical data used for future projections. While past performance doesn’t guarantee the future, that’s the only thing we have to go by. So, if you want to do this exercise on your own with different assumptions than the above, choose a retirement calculator that uses historical data and not Monte Carlo simulation, because the latter is random and doesn’t consider a realistic sequence-of-returns.

What historical data-based calculators like FIREcalc or cFIREsim do is that they assume the future, while it cannot be exactly like the past, is no worse than the past. So, instead of making random assumptions about returns and volatility (which Monte Carlo simulators do), these calculators use actual data. In their own words:

FIRECalc makes a single fundamental assumption: If your retirement strategy would have withstood the worst ravages of inflation, the Great Depression, and every other financial calamity the US has seen since 1871, then it is likely to withstand whatever might happen between now and the day you no longer have any need for your retirement funds.

If the market does no worse than the great depression, 1970’s stagflation, or the dotcom bust, will my money last in retirement? At it’s most basic level, cFIREsim uses historical stock/bond/gold/inflation data from 1871 to present, and calculates how your portfolio would have fared throughout history.

By using the same financial market assumptions for all three cases, we will eliminate market performance as a variable in drawing relative conclusions. Remember, whatever worse case the future throws at these early retirees are presumed to be no worse than all that we have seen since 1871, as mentioned above.

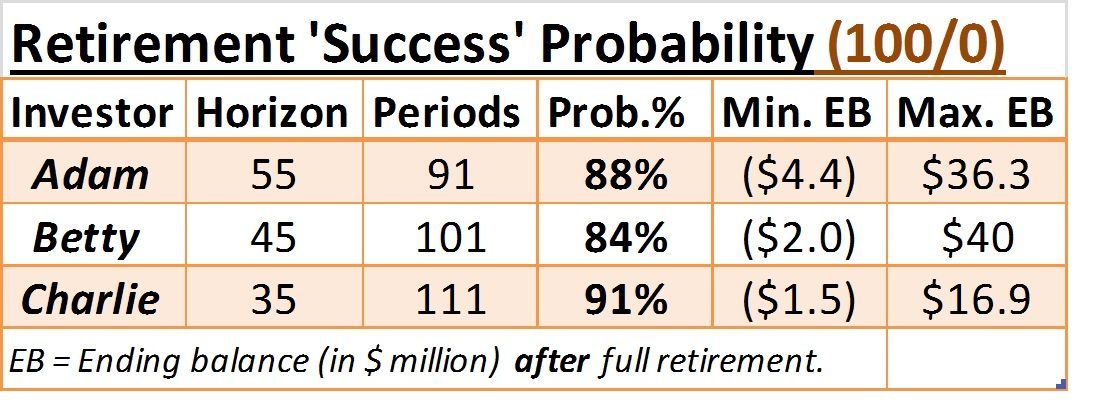

The Case for 100% Equities

For the purpose of this calculation, ‘probability of success’ means the likelihood of you enjoying your full retirement without running out of money. ‘Periods’ refers to the number of periods or time-spans each retirement scenario was considered for the modeling. Note I have only included minimum and maximum ending balances (EB) in the table and not ‘average’, because in simulations involving 100 trials or so, average is meaningless as it is just one scenario among all the others. Similarly, don’t pay too much attention to individual values of EB, but rather relative trends.

There will always be scenarios with negative EB unless the probability of success is 100%, so don’t worry about it. Real life offers many adjustments even in worse cases. So, negative EB is expected in this kind of simplistic model study where we blindly assume increasing withdrawals each year regardless of what the market is doing. You can increase ‘success’ probabilities by simply reducing initial withdrawals till the model spits out 95% or 99% success, but if you are already near 90%, that doesn’t matter much.

See how the probabilities of retirement success bunch up around 90% for all three. In other words, whether you are looking at a 35-year or 55-year retirement horizon, you are not terribly different from a modeling success perspective, which is a vindication of the ‘4% rule‘. In case you are wondering why there is a drop to 84% for the 45-year retirement period, it is only because of the present time frame we are doing this analysis. In other words, the starting periods of 1965-66 (worst year to begin retirement) and the difficult 1970’s have a slightly higher impact on the failure rates of a 45-year horizon as they miss out on the earlier booming 1950’s and early 60’s that a 55-year planning horizon considers. In practical terms, this difference is not so significant. So, Betty will do no worse than Adam.

See how the probabilities of retirement success bunch up around 90% for all three. In other words, whether you are looking at a 35-year or 55-year retirement horizon, you are not terribly different from a modeling success perspective, which is a vindication of the ‘4% rule‘. In case you are wondering why there is a drop to 84% for the 45-year retirement period, it is only because of the present time frame we are doing this analysis. In other words, the starting periods of 1965-66 (worst year to begin retirement) and the difficult 1970’s have a slightly higher impact on the failure rates of a 45-year horizon as they miss out on the earlier booming 1950’s and early 60’s that a 55-year planning horizon considers. In practical terms, this difference is not so significant. So, Betty will do no worse than Adam.

Where the difference really crops up is in the ending portfolio values. With longer retirement horizons and with 100% stock allocation, you have a real chance of leaving a large legacy (residual net worth), for charities or inheritances. Of course, we saw how a 100% stock portfolio is the most efficient, and gives the highest expected return, if you can tolerate wide fluctuations in portfolio value (in other words, if you can handle “risk“, as the mainstream calls it). This is what fellow blogger GoCurryCracker means when he says, Posterity will benefit tremendously from our tolerance for risk. Despite lost opportunity cost of 10-20 years of earned income they have forgone by extreme early retirement, due to their tolerance for higher market volatility, Adam and Betty (along with GoCurryCracker) will do just fine compared to Charlie.

What Mainstream Finance Misses

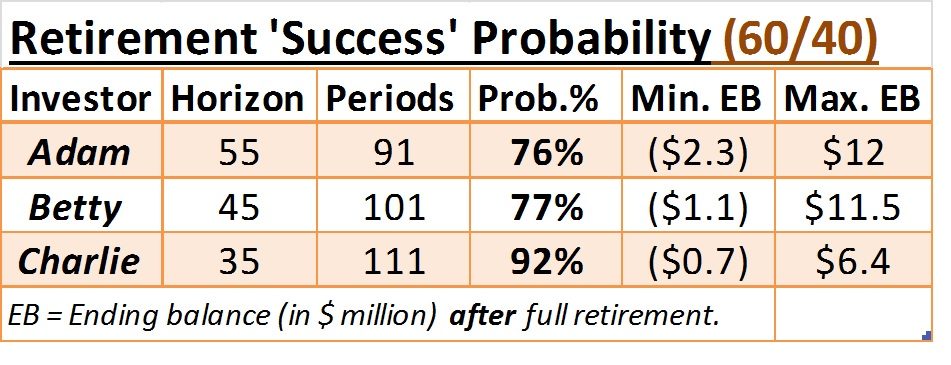

For the same investors, shown below are results where the investment mix is changed from 100% stock portfolio to a more traditional 60/40 portfolio (60% stocks and 40% bonds) as advised by many financial planners. To eliminate the impact of fees on results, this option also assumes the same, ultra low 0.1% annual fees. All other factors are also the same as in the first case.

Now, significant differences crop up between Charlie and Adam/Betty. For a portfolio that gives a ‘smoother’ ride because of sizable bond allocation (less volatility), the price you pay for longer-term horizons (45 or 55 years) is lower probability of success. In other words, the odds of Adam and Betty running out of money is about one in four, which should worry them. Charlie will not only have a smoother ride but is likely to do fine over the 35 years the portfolio is expected to work for him.

All is not lost for Adam or Betty. The value of a sizable stock (60%) portfolio shows up if you allow more of your money to work in the market. So, I did a calculation for Adam to see at what initial withdrawal (adjusted for inflation) will Adam have the same 88% probability that he has in the first table above at 100% stock allocation. Guess what the answer is?

$37,300! For less than 10% reduction in initial annual spending, Adam can significantly improve the probability of success of his retirement. You can also achieve this in another way. Adam or Betty can still withdraw the same $40,000 initially as Charlie does at the beginning of retirement, but they must forego inflation increases for 3-5 years when times get tough (say, the portfolio drops in value by 30% in one year and takes the next 3 years to recover). Charlie, on the other hand, doesn’t have to forego any inflation raise and can largely forget about the market. This is where his smaller time horizon comes to his advantage.

Bottom line

If you withdraw 4% or less from your ‘aggressive’ 100% stock portfolio, then retirement spans beyond 30 years don’t matter. If you want a smoother ride by having 40% bonds in your portfolio, then your retirement span matters a lot. Still, if you can live on 3.7% or less of your 60/40 portfolio (instead of 4%), you will likely do fine even if you have a 45-55 year retirement span. What’s helping all the cases here is ultra-low fees at 0.1%. Beware: If you are investing at 1% fees, you must subtract this from the above withdrawal rates – this fees will eat up 25% of your annual withdrawal right there, ouch!

The big difference, though, is in ending balances. In one case, your legacy can build a new hospital and in another case, maybe just a hospital wing? Your descendants will either become the next Rockefeller or just a ‘modest’ millionaire. Journey safely, my 10! friends.

Raman Venkatesh is the founder of Ten Factorial Rocks. Raman is a ‘Gen X’ corporate executive in his mid 40’s. In addition to having a Ph.D. in engineering, he has worked in almost all continents of the world. Ten Factorial Rocks (TFR) was created to chronicle his journey towards retirement while sharing his views on the absurdities and pitfalls along the way. The name was taken from the mathematical function 10! (ten factorial) which is equal to 10 x 9 x 8 x 7 x 6 x 5 x 4 x 3 x 2 x 1 = 3,628,800.

6 comments on “FIRE: How Long vs. How Much”