This article covers total return performance in dividend investing vs. indexing. If you landed here directly, you may want to read the series in sequence to follow this important subject for investors: Part 1, Part 2, Part 3 and Part 4 are preludes to this article. For easy reference, the entire series is organized in a single page.

We will start with the most cited (and valid) risk from Indexers regarding the dividend growth investing (DGI) method. That is, DGI investors are at risk of lagging the equity index’s total returns. The roots of this risk are covered in Part 1 of this series. Briefly, most professional investors are unable to beat their benchmark index over the long-term. We examined why this is so, so I will not repeat the points here. Some of these risks remain even for individual investors who pick dividend stocks. While you won’t have fees and other performance drags that professional money managers face, the biggest determinant of your return is stock selection.

Where DGI Goes Wrong

If you embrace a DGI approach, do so with eyes wide open on both its benefits and limitations. If you do DGI with a goal to “beat the market”, your objective isn’t aligned with DGI strategy at all. Those who think DGI makes them a great stock picker for beating the market will be disappointed. DGI is considered a low turnover, conservative strategy even among the stock picking world. It has elements of ‘value investing’ that help in total returns but index out-performance is not guaranteed. Those who choose DGI thinking it will help them generate both more income and beat the index run the risk of achieving neither. They will then abandon the strategy mid-way and neither benefit from the compounding of dividends nor achieve a competitive total return.

Global equity markets averaged almost 100 million daily trades in 2015, valued nearly at $450 billion a day, according to Dimensional Fund Advisors. Consider SPY, an exchange-traded fund that tracks the S&P 500 index. In 2016, it averaged 104,904,708 shares traded daily, meaning over $22 billion worth changed hands. For the S&P 500 stocks, the daily average for 2016 was 641,398,857. Just one stock, Apple (AAPL), trades more than 30 million shares every day. This frenetic trading activity keeps the market largely efficient, though mis-pricing (from a value perspective) does happen.

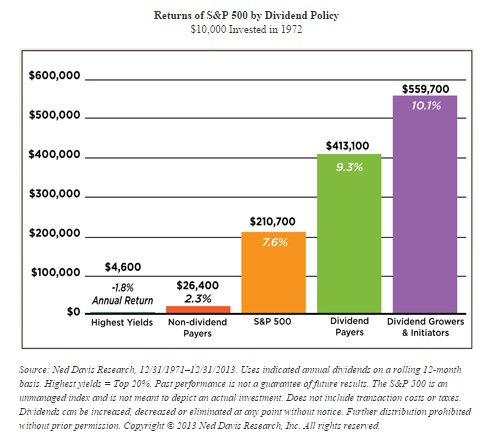

Bottomline: Remain humble about your investment strategy and stay focused on why you are following it. Work to reduce the risks in your dividend portfolio rather than attempting to do something (like beat the index) with DGI that it is not intended to do, though it can happen; as the Ned Davis study showed (summary chart follows).

Index Lag Can Happen…

Despite the assurance of Ned Davis Research, it is entirely possible your portfolio of dividend paying/growing stocks may lag the S&P 500 index. It depends on how your stock portfolio performs and is somewhat correlated (as we saw earlier) with how high your dividend yield is. If you put together a portfolio of 6% or higher dividend yield, when the broader market (S&P 500) is yielding 2%, you are likely to experience under-performance in total returns over the index over the long-term because market doesn’t offer very high yields without reason. Remember the ‘rule’ we mentioned earlier, higher the dividend yield, slower the future growth. A parallel to this in the indexing world is: higher the initial withdrawal rate, lower the terminal value of the portfolio. But a dividend portfolio of say 3-4% yield may be competitive with the index in total performance.

Celestially blessed index lag?

There is no economic law about the number of days the earth takes to go around the sun. Yet, performance returns are always benchmarked on the Gregorian calendar. It is possible for a stock to lag an index from Jan. 1-Dec. 31 of a year, and yet beat the same index when measured Feb. 1 till Jan. 31 of the following year. Same 365 days, different starting and ending points. Heck, even our 365-day calendar is not accurate, and it needs a one day adjustment every 4 years to catch up to the real orbiting time of the earth.

Okay, some holy cows cannot be questioned, so we will respect the eternal bond between the stock market and the celestial solar calendar.

Let’s say, Irene is an indexer whose portfolio has 2% yield and is expected to earn 8% annualized return over the coming 30 years (this is essentially same as S&P 500 index). Note that the 8% return includes the 2% dividend yield. For this example, we will assume that Irene re-invests her dividends back into her index portfolio. Betty is a DGI investor with 3.5% dividend yield, who also re-invests her dividends in her portfolio that generates total return of 7% over 30 years (this includes the 3.5% yield). In other words, Betty’s total return lags Irene’s by 1% every year. Recall the Ibbotson data we cited in Part 1, of the total 7% for Betty, the 3.5% dividend yield is ‘stable’ and 3.5% capital appreciation is ‘fickle’ (in other words, subject to market conditions). Let’s assume both investors start with the same $500K portfolio as we assumed earlier. This doesn’t matter – the conclusions will hold no matter what portfolio size you start out with.

After 30 years, Betty will have: $3.81 million in her portfolio. And Irene will have $5.03 million, a massive $1.2 million more than Betty. These figures are 30 year compounded returns, at 8% and 7% for Irene and Betty, respectively.

There is no two ways about it – higher portfolio return of Irene will result in higher terminal value. This is math and you can’t argue with it.

…But It’s Less Important Than You Think

The math is clear but it ignores investor psychology.

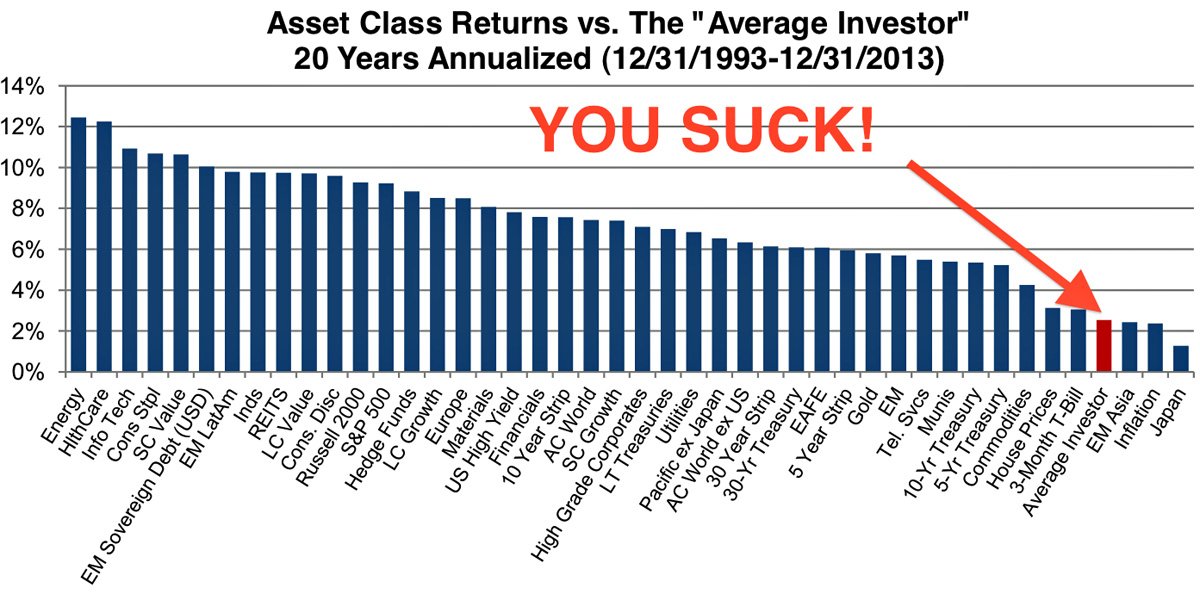

Fidelity did a study of its clients to identify the best performing investors. Guess what? The best ones were either dead or long forgotten that they even had accounts with Fidelity! In other words, ‘buy and hold’ works.

The worst enemy for an individual investor is likely himself or herself. The average investor did far worse than any investment index, including any sector focused funds (which indexers accuse DGIers of not being diversified enough).

Indeed. (source: Richard Bernstein Advisors LLC)

What this means is that the ‘index lag’ only applies if you stayed invested, through thick and thin, in the S&P 500 index. Then, you could’ve realized the 9% annual return that the chart shows for the 20-year period. Instead, the fear and greed psychology that dominates individual investors cause many to move in and out of markets, often at the wrong times. This leads to horrendous actual returns of less than 3% annualized over a 20-year period.

So, any investment strategy that helps you stay invested is likely to do you good. This is where DGI outshines a pure indexing strategy. Since you are steadily receiving dividend income – through thick and thin – during the course of your investing life, your need to sell stocks at the bottom is greatly diminished. Since dividends are continuously and periodically generated, you are likely to even purchase stocks using your dividends during bear market conditions, resulting in higher dividend income (remember the internal compounding example in Part 3?) and possible long term outperformance in total returns as well.

So, any investment strategy that helps you stay invested is likely to do you good. This is where DGI outshines a pure indexing strategy. Since you are steadily receiving dividend income – through thick and thin – during the course of your investing life, your need to sell stocks at the bottom is greatly diminished. Since dividends are continuously and periodically generated, you are likely to even purchase stocks using your dividends during bear market conditions, resulting in higher dividend income (remember the internal compounding example in Part 3?) and possible long term outperformance in total returns as well.

Therefore, DGI is suited to a more conservative (within the 100% equity risk profile) investor psychology. This is because you are receiving periodic income (which is positive and likely growing) regardless of the broader market conditions. This creates a virtuous feedback loop compared to an investment philosophy where a statistically-derived safe withdrawal rate dictates liquidation of stocks to support spendable income, regardless of overall market conditions. Also, you can assemble your DGI portfolio to have less volatility (beta) than the index by a higher allocation to stocks in consumer staples and utilities sectors. Such a portfolio declines less during bear markets as these are ‘defensive’ sectors that hold up well even in recessions. However, it is likely to lag the S&P 500 index during raging bull markets. This is why such a DGI portfolio, despite being 100% stocks, is still seen as ‘conservative’.

A stock that pays you periodically is likely to be held longer even if its price languishes or declines than a stock that doesn’t pay you a penny in dividends. Investor psychology to hold- because you are getting paid to do so – is understandably stronger. The index also pays you dividends but since your SWR is independent of dividends generated, you have no correlation between the two for setting spending targets.

If you can hold the index fund through a 40-50% bear market draw down without batting an eyelid, then you don’t need the positive reinforcement of periodic dividends. But if you need the ‘cushion’ of a sizable bond/cash portion to handle market turbulence, then your own index portfolio will lag the equity index performance over long term. In the previous example, all it takes for Irene’s total returns to match Betty’s is for Irene to hold 15-20% bonds in her portfolio.

On the other hand, the positive and periodic dividends flowing from the DGI method allows you to maintain a higher equity allocation than a typical stock/non-stock index portfolio. This alone will make a big difference to your long-term returns. How, you ask? It’s because asset allocation drives more than 90% of the total investment returns. So, you can enjoy both higher current income and higher long-term portfolio value!

Reward for maximizing portfolio value?

Even if you count yourself among the lucky dead dedicated index investors, the performance lag only comes into play over a long period of time. In the meanwhile, the dividend investor has been enjoying higher current income without having to worry about portfolio longevity because no shares are being sold. Even if the indexer reminds him that “hey, you are doing this at the cost of a lower future portfolio value”, he may not care because income enjoyed throughout retirement is far more important than getting to the highest portfolio value. There are no rewards for being the richest man in the graveyard.

Suffering a very low withdrawal rate throughout retirement to help maximize portfolio’s terminal value doesn’t make sense to me. It’s like saving sex for old age, as the inimitable Warren Buffett says!

Also, we forget that the index is not some static thing. The composition of stocks in S&P 500 index are chosen by a committee. Every year, stocks are added and removed from the index. If the index itself is changing, what are you comparing it to? Jeremy Siegel pointed out that buying the original S&P 500 (when it was first created) and holding it forever would have given you an extra 1.5% per year return over a ‘changing’ S&P 500 index fund. This is because the lower valuations of companies leaving the S&P 500 make them undervalued, and generate better total returns than the index in the future.

Another point to consider if your DGI portfolio of say, 30 stocks, has 25 from U.S., 4 in international developed countries and 1 company from an emerging market that you believe in, is S&P 500 even a relevant index for you? A better benchmark index may be a composite of 80% SPY, 15% EFA and 5% EEM. This benchmark would be closer to your DGI portfolio than the S&P 500 index.

Yes, index lag is a real risk for a DGI investor, but what is the index you are comparing to? If maximizing portfolio value is your main goal, then DGI is not for you. Also, consider how important that goal is from the perspective of your long retirement horizon where you need real continuous income along the way and the benefits of enjoying that income when you are relatively healthy and younger (<70 years) while staying in an equity-heavy portfolio.

We will bring this series home in the next article by seeing if we can have the best of both worlds – DGI and Indexing.

Raman Venkatesh is the founder of Ten Factorial Rocks. Raman is a ‘Gen X’ corporate executive in his mid 40’s. In addition to having a Ph.D. in engineering, he has worked in almost all continents of the world. Ten Factorial Rocks (TFR) was created to chronicle his journey towards retirement while sharing his views on the absurdities and pitfalls along the way. The name was taken from the mathematical function 10! (ten factorial) which is equal to 10 x 9 x 8 x 7 x 6 x 5 x 4 x 3 x 2 x 1 = 3,628,800.

5 comments on “Dividend Investing vs. Indexing – Part 5”