May not be as easy, but comes close if you put some effort into it.

There are many seekers of financial independence and early retirement (FIRE). Many depend on financial advisors to help them reach a comfortable retirement. To reach FIRE faster, however, you may have to fire your financial advisor!

I have always managed my finances on my own, and you can too.

For those with any college education, and especially for those with a STEM degree, there is nothing in the world of finance beyond the grasp of your understanding. Even college isn’t required in many cases, high school level math and common sense is more than enough to master many financial topics.

The financial advisory community, especially those that charge 1+% fees for managing your hard-earned assets, is taking a huge share of your wealth. Much more than what many realize. We will walk through a realistic example below.

Let’s take the case of three investors, Adam, Betty and Charlie – the same characters who feature in my investing series. Let’s assume they are all 30 years of age, have $100,000 to invest and are able to invest an additional $500 a month from their earnings.

Adam believes that personal finance is complicated so he is better off with an advisor, who he pays 1% as fees to help relieve him from the hassles of managing his money. This way, he figures he can focus on his work and family. Since the fees are a percent of his asset size, Adam believes this better aligns the financial advisor’s interests with his own.

If the person Adam chooses is a decent financial advisor, he might recommend good quality mutual funds that have 0.63% expense ratio. Why did I pick this specific figure for expense ratio? This expense ratio is the average of all equity mutual funds (both active and passive), based on 2016 study by Investment Company Institute.

There are many people who would agree with Adam when it comes to finances. They would rather focus on their work and increase their income rather than worry about managing their investments or other financial matters.

Betty is another investor who believes she also needs help but has read finance articles (including this website) to know that she should invest in passive index funds or a diversified portfolio of high quality dividend growth stocks, at low cost. Still, she feels it is useful to hire an advisor, and does so for a fixed fees of $1000. In return, the advisor will give Betty a complete investment plan and advise on other financial matters for her to follow on her own. The plan for Betty is to put together a passive index fund portfolio at 0.1% expense ratio.

In other words, this is the ‘advisor-lite’ version. This can be a sensible route for many, and one that I recommend for most DIY investors because you have another expert giving you an unbiased opinion, based on your situation. Even if you are fully DIY with your finances, having this second set of eyes give an opinion can be valuable.

For the second year onward, say Betty’s advisor charges only $300 (going up just 3% annually, because even the advisory rates must keep up with inflation) to ensure Betty is on track. This annual review is for the advisor to suggest tweaks, if necessary.

Betty pays only 3 of these Benjamin’s per year to keep her on track. Not a bad price to stay the course.

Charlie – an avid reader of Ten Factorial Rocks and several other personal finance books and websites – believes he can invest efficiently on his own. He chooses to invest passively, incurring a tiny 0.1% expense ratio for a diversified equity fund portfolio.

He could also choose to invest in a portfolio of dividend paying stocks that track market returns, in which case, let’s assume for the sake of simplicity, the same 0.1% index fund fees is what he incurs in brokerage commissions (though in reality, for sizable portfolios, low trade dividend stock investing is cheaper than indexing).

Since asset allocation determines more than 90% of investment returns, we will level the playing field between Adam, Betty and Charlie by assuming they all invest 100% of their portfolio in U.S. equities (despite the different routes they follow). So, there is no difference between them in the category of assets invested.

Therefore, at a gross level, let’s say their returns are the same 6%, annualized. Given the current market valuations, I don’t feel comfortable assuming any higher return figure than 6%, despite some personal finance authors assuming 8%, 10% or even 12% annualized from stocks!

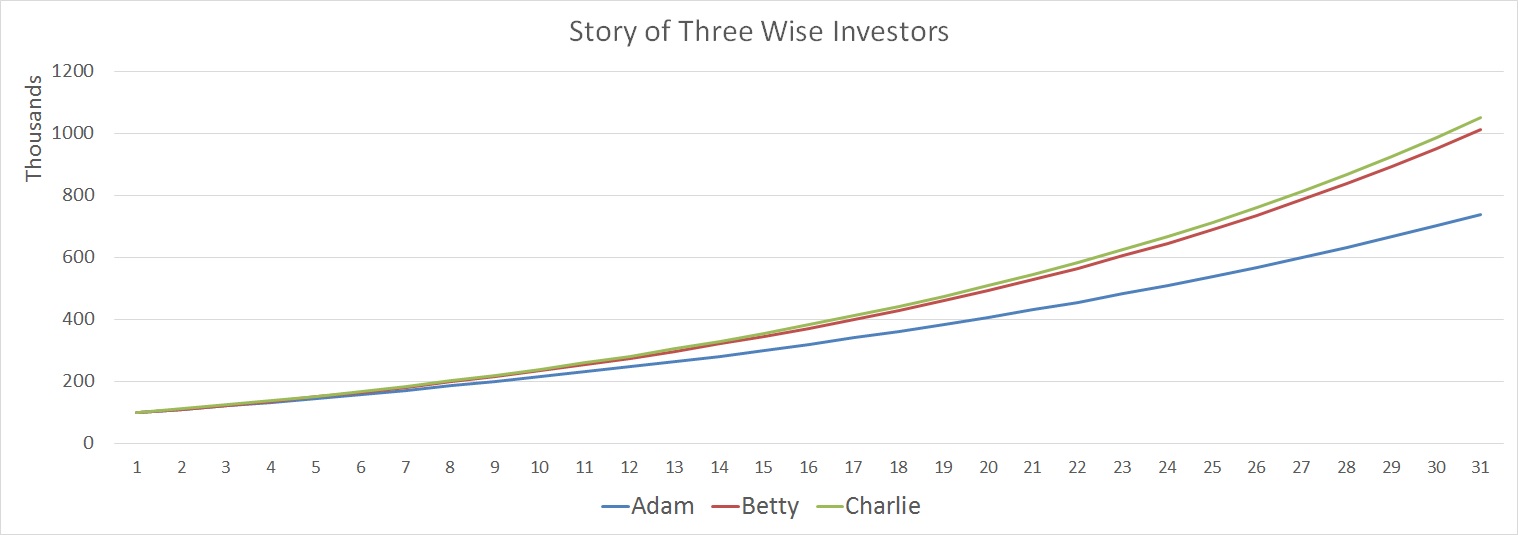

Here is the investing journey for Adam, Betty and Charlie over 30 years for 100% equity portfolio with the above assumptions.

Tale of 3 wise investors.

First, you will notice that I called them all “wise investors”. That’s because all of them recognized the value of investing early, started with a sizable investment fund of $100,000, and all were smart enough to recognize that stocks are the best asset class for long-term wealth creation.

But there are different degrees of “wise” as we all know.

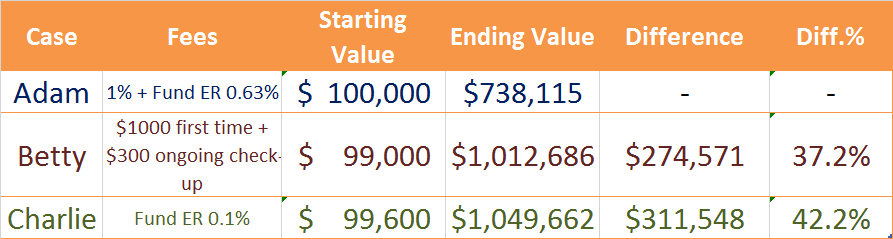

Adam pays the highest price among all investors for his hassle-free approach to investing by hiring a financial advisor who charges a typical 1% of assets, and who recommends a typical equity mutual fund with an average 0.63% expense ratio (ER).

He could’ve ended up far worse, had he chosen a financial advisor who charges more than 1% of assets (not uncommon) who may have put him in equity funds with expense ratio of over 1% (not uncommon).

Both Betty and Charlie fare far better than Adam, as the chart and the summary table below show.

Ready to fire your financial advisor yet?

Betty ends up with 37% more money than Adam, and Charlie ends up with 42% more. These differences are massive, and amount to multiple-hundred thousand dollars, as the figures show.

Put another way, even the average cost advisor and his not-too-expensive recommendations have gobbled up nearly a third of the total money over the 30 year investing horizon! So much for “tiny” 1% fees, right?

A key question here is whether Adam was fully aware of this going in. Most investors are like Adam – they usually aren’t.

Fees that start out in tiny $1 bills quickly compound to these types of bills!

What is interesting to recognize is that even among Betty and Charlie – who both embraced passive investing at low fees of 0.1% ER – there is a significant difference of almost $37,000 in ending portfolio value.

First, Betty starts with $1000 less than both Adam and Charlie – that’s the initial advisory fee she paid. Also, Betty continues to pay a fixed fee of $300 each year (inflation-adjusted) for portfolio check-up every year with the advisor (despite having invested in the same low cost mutual funds as Charlie).

Since Betty invested in low cost funds and there are no percentage ongoing fees like Adam, she quickly overtakes Adam (by Year 3). But she cannot catch up with Charlie over the entire 30 year period.

The total fixed fees paid by Betty over the 30 years works to $15,700. Betty actually has a good deal on the fixed-fee advisory service she used – many other investors pay lot more than $300 for annual check-ups.

Still, she ends up with nearly $37,000 less than Charlie because every year, these fees – however tiny – are removed from the portfolio balance which makes the compounding base a bit smaller than Charlie’s for the same year.

Now, I don’t want to over-emphasize the difference between Betty and Charlie – both have done very well. The difference between them is minuscule for their asset size.

Some eagle-eyed readers will observe that Charlie starts not with $100,000 but $99,600, that is $400 less. If you already noticed that in the table above, good for you! Do you want to know why?

I deducted $400 from Charlie’s starting portfolio to pay for a comprehensive investing course, that covers every aspect of personal finance, starting from savings, investing, asset allocation, insurance, real estate and even estate planning. Every one of these dimensions of personal finance is important to grow your net worth and to build a moat around it.

I have reviewed several investor courses over the years. I can hardly think of a better, comprehensive course than White Coat Investor’s (WCI) course – Fire Your Financial Advisor!

This self-paced course will make you not only become like Charlie, but also a better informed investor than many so-called advisors and financial planners. I have reviewed this course end-to-end and find it to be crisp, comprehensive and clear.

This course is not for everyone. It is meant for reasonably high income professionals (at least making $60,000 a year) who want to be a do-it-yourself investor and handle all aspects of their financial life.

The $500 course fee is worth every penny as this one-time investment will save you tens of thousands of dollars compared to even other passive index investors who use low cost fixed-fee advisors. And it will save hundreds of thousands of dollars over financial advisors who charge even one percent of your assets as their management fee.

WCI also offers a no-questions-asked, 7-day moneyback guarantee. So, try the course and decide for yourself – totally risk-free. You will find yourself referring to it often as you execute a solid financial plan.

I will also offer a 50% discount for the first personal consultation with me for those who have completed this course using my referral – this alone pays for big chunk of the course cost!

Why do I offer this? Because my work in personalized consulting becomes easier if you become a savvy investor. So, you can choose to be either Betty or Charlie!

I actually want to reduce my consulting work so this course helps in cutting down on my investment-related consultations. This allows me to focus more on income generation and other lifetime value strategies for those who want to work with me.

Ending up with more assets than other investors allows you, among other things, to live it up in retirement!

You can learn more and sign up using this link or click on the course banner above or on the side panel. (Disclosure: This site will receive a small affiliate commission if you use this link, to help keep the lights on at TFR website. That is hardly any reason for me to recommend it. My discount offer negates any gain from this commission so this isn’t a driver for me. There are several ‘better paying’ investor programs who reach out to me periodically that I think aren’t worth even a fraction of what they charge).

Take the course, and see for yourself. Your future self will thank you!

Raman Venkatesh is the founder of Ten Factorial Rocks. Raman is a ‘Gen X’ corporate executive in his mid 40’s. In addition to having a Ph.D. in engineering, he has worked in almost all continents of the world. Ten Factorial Rocks (TFR) was created to chronicle his journey towards retirement while sharing his views on the absurdities and pitfalls along the way. The name was taken from the mathematical function 10! (ten factorial) which is equal to 10 x 9 x 8 x 7 x 6 x 5 x 4 x 3 x 2 x 1 = 3,628,800.

9 comments on “Fire Your Financial Advisor!”