Warren Buffett’s legendary investment skills, folksy wisdom, dedication to shareholders combined with a frugality-effacing, witty personality have made him a darling of the global investing community (except Wall Street firms, which he deservedly chides). Many of us love to read his legendary annual letter to shareholders that he publishes in the latter part of February each year, recounting the prior year’s achievements of Berkshire Hathaway and his outlook for the future.

Mr. Buffett has been publishing these letters for over 50 years, and each one is a masterpiece in business thinking with nuggets of human psychology. Reading these letters and applying them in your life is worth more than even the most expensive MBA in the world. While he is too young for it now, I really hope my son grows up to read these letters and apply their wisdom. They are a fascinating narrative of clear thinking, piercing logic and valuable observations of human psychology – all delivered in a form that only Mr. Buffett can.

Fees are terrible…duh!

In his recent 2016 letter, Warren Buffett blasts the entire hedge fund industry for excessive fees that cause poor investment returns. He qualified that he doesn’t mind paying fees if they deliver value, which they often don’t. He also praised Jack Bogle as a hero of the average investor by developing the world’s first index fund. Vanguard’s growing success today is clear proof of what Jack Bogle did. The main reason why Warren Buffett is winning the $1 million index fund vs. hedge fund bet (with 9 out of 10 years completed) is the extraordinary fees levied by the active funds. It is not that the investments went wrong, but the fees killed the net returns.

“Consequently, I estimate that over the nine-year period roughly 60% – gulp! – of all gains achieved by the five funds-of-funds were diverted to the two levels of managers.” Warren Buffett (2016 Letter to Shareholders, page 23).

If 60% of the gains from S&P index’ compounded annual return of 7.1% over 9 years is gobbled up by fees, what you have is a paltry 3.3% return. When the high fees are applied to index return, more than half of the return is swallowed by fees! We saw in Part 1 of our investing series how even a reasonable active management fees of 0.7% requires the fund manager to beat the index by 10% every year to counter the effect of fees. So, imagine the severe handicap these hedge funds have.

To bridge the 3.8% ‘gap’ (7.1% – 3.3%) in annual return between S&P 500 index fund versus the competing hedge fund, the active fund would have had to beat the index by the same gap, that is, achieve a 10.9% annualized return to have the same net return as the index fund. This is 53% higher than the actual index return!

Even Warren Buffet did not accomplish this feat year-after-year over the last 9 years (which includes the 2008-09 recession), so a high-fee hedge fund has a snowball’s chance in hell. Beating the index by over 50% can happen in a year or two with some concentrated bets by brilliant (and lucky) investors, but over 9-10 years? Just impossible! You can see why Mr. Buffett was very confident of winning his bet from the start.

Bet against Warren? It’s a sucker’s bet. (source: Berkshire Hathaway 2016 shareholder letter)

While many will see Mr. Buffett’s 2016 letter as yet another endorsement of low cost index investing, there is a more subtle message buried in this letter and in his letters of earlier years. It is possible to earn returns competitive to an index or even beat the index for an individual investor, but using an overpaid asset manager is not the route. That message appears within these lines:

“So that was my argument – and now let me put it into a simple equation. If Group A (active investors) and Group B (do-nothing investors) comprise the total investing universe, and B is destined to achieve average results before costs, so, too, must A. Whichever group has the lower costs will win.” Warren Buffett (2016 Letter to Shareholders, page 24).

Since dividend growth investing can have even lower costs than indexing for a sizable portfolio, you have the first tailwind in favor of assembling a portfolio of high quality dividend paying stocks that have thrived over several business cycles. This is for those who choose to think beyond indexing.

Graham was just the beginning

Warren Buffett loves dividends flowing in from his investments as he has said before, even if Berkshire doesn’t pay one. That’s because he feels he can allocate capital better than Berkshire investors who receive the dividends. In his own style, he marries both dividend investing and value investing philosophies. This is evident from his love of cash dividends coming back to Berkshire for future investments and his love of insurance ‘float’. So, the subtle message in Buffett’s letter should be motivating to a long-term dividend growth investor by selecting a diverse mix of leading companies across industries that have competitive advantages in their own sectors. That’s not the message many will read. Remember the main reason why an index fund beats active funds? It’s the fees! Fees are practically zero to a self-directed dividend investor who trades very little.

Have you wondered who guided Warren to this style of investing (in 1980’s from his previous purely value-oriented small company investing approach)? For a man who is as intelligent, successful, connected, well-read and resourceful as Warren Buffett, we should understand the two people he keeps referring to as his mentors and counselors.

Ben Graham: The ‘father’ of value investing.

One is, of course, Prof. Benjamin Graham (author of the investment classic The Intelligent Investor), who Warren learned personally from at Columbia University. As history shows, Graham inspired Warren Buffett towards the ‘net net’ style of investing – that is, acquiring companies at or below net assets on their balance sheet, and selling them off profitably later. Warren Buffett later called this ‘cigar butt’ style of investing – mediocre/declining companies thrown away like a cigar butt. Buffett will buy them at rock-bottom prices knowing they still had a ‘puff or two’ left, and then realize value in those last puffs. Buying mediocre companies at dirt-cheap prices and selling them (or their assets) later at a profit works but had Warren remained here, he wouldn’t have become the legend he is today. That brings us to the next major influence in his journey.

An Oracle behind The Oracle

That is his long-time partner and friend, Charlie Munger. While the world is fascinated with Warren Buffett, I find it more fascinating to study Mr. Munger. It started by wondering why Warren defers to Charlie for important decisions. The answer is in Charlie’s ability to have a “latticework of mental models” that enable him to take better decisions than many. Like Mr. Buffett, Mr. Munger is also a voracious reader but even more so, he is able to continually add to his deep inference-oriented thinking ability that he uses to enhance the quality of decisions he makes. Charlie is credited with introducing Warren to the world of large scale, widely entrenched and enduring long-term businesses with strong brands like Coca Cola, Wells Fargo, IBM, American Express etc. These are mega-cap dividend growth names, some or all of which are part of many dividend investor portfolios.

Those who haven’t read should study Mr. Munger’s speech on “The psychology of human misjudgment” to Harvard Faculty Club in 1994. While not appearing as eloquent as Warren, Charlie holds his own in every speech. I particularly think that speech is the best gift to every university graduate. In fact, the transcript should be stapled along with every degree or diploma. Universities have become factories that turn out narrow specialists and emphasize rote-learning so much that the ability to do cross-functional thinking is practically dead. Hear the full speech at the link at the end of this post – it’s worth the one hour you spend.

I give invited lectures to a few leading universities. I cherish these opportunities because I get to interact with bright, young minds and also learn from them how to see the world through new ways and understand what catches their fancy these days. I also find some disappointing trends. The world of specialized online forums and targeted social media have created ‘online cocoons’ inside which many people stay and remain comfortable. With distance no longer an issue, it is possible for esoteric interests across the world to congregate and ignore all others outside their interests.

For example, a chameleon patterned Mohawk hair style enthusiast from Rio de Janeiro, Brazil can connect with a person with the exact same interest in Osaka, Japan who connects with a similar dude in Reno, Nevada who has a YouTube video series on how to keep the chameleon looking lively on that Mohawk. Maybe only 200 people in the world like the same thing but you can bet they are all passionate about it and have an online forum to connect and remain closeted within. Specialization even within very narrow interests, you get the ‘brush’ of the idea, right? 🙂

For example, a chameleon patterned Mohawk hair style enthusiast from Rio de Janeiro, Brazil can connect with a person with the exact same interest in Osaka, Japan who connects with a similar dude in Reno, Nevada who has a YouTube video series on how to keep the chameleon looking lively on that Mohawk. Maybe only 200 people in the world like the same thing but you can bet they are all passionate about it and have an online forum to connect and remain closeted within. Specialization even within very narrow interests, you get the ‘brush’ of the idea, right? 🙂

Bringing the wrong tools?

Many people evaluate every new subject from the narrow prism of their core expertise that they trained for. This was clear even in the questions I got after a recent invited lecture to an MBA class. It’s like an accountant who doesn’t believe in strategy or a technology expert doesn’t value salesmanship, and a salesman who uses consumer psychology but yet, thinks of psychologists as quacks who failed to become real doctors! They evaluate a multidisciplinary decision (like investing) through the narrow eyes of one specialty which they are most comfortable with. All this reminds me of the saying “If all you have is a hammer, every problem looks like a nail.“

From cigar butts to ‘moaty’ companies

Charlie Munger: The catalyst behind THE Oracle?

Charlie Munger has been my inspiration for over a decade, sometimes even more so than Warren Buffett because he gives actionable guidance on how to think while Buffett talks eloquently about what to think and when to think. This is also important but without learning how to think first, you can’t learn the others well. Charlie is known to hold an arsenal of more than 100 mental models in his head. He layers all new experiences and information on them to continually refine and make decisions. I only do a fraction of that but even that has made a great difference to my business career and investing results. When told about investing with advanced computing methods, Buffett says, “no computer can ever replace Charlie.” Adds Bill Gates about Charlie: “He is truly the broadest thinker I have ever encountered.”

Among Charlie’s greatest influences on Buffett, by his own words, is getting Warren to go beyond the ‘cigar butt’ style of investing into high quality, large companies with enduring business models. This is allied to his philosophy of holding stocks “forever”. You certainly don’t hold ‘cigar butts’ forever. Large cap, dividend paying and steadily growing companies with a strong moat are the stocks to hold forever.

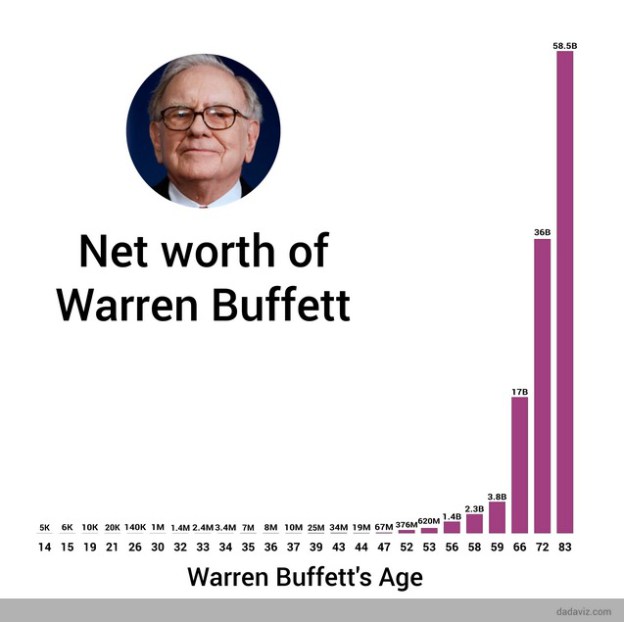

So, what kind of results did Charlie inspire Warren to achieve? How does 99% sound? Of Buffett’s wealth creation track record, over 99% of the total wealth was created after he turned 50, which is when he embraced the large-cap value investing style with growing dividends. This wealth has come from his focus on the types of companies mentioned earlier, while the periodic dividends flowing back to Berkshire have compounded further in other stocks.

This picture is worth 60 billion words. (source: valuewalk.com)

As an example, the 400 million shares of Coca Cola (9.5% of the entire company) he now owns (purchased in late ’80s at a total cost of $1.3 billion) is now worth $16.58 billion. Importantly, its quarterly dividend of $0.37/share (raised recently from $0.35) will ensure Berkshire receives $592 million in dividends alone in 2017, at an astronomical yield-on-original-cost of 45.5%! Over time, Berkshire has recovered several times its investment costs in Coca Cola and other companies in dividends alone. This kind of return comes from long-term (multi-decade) compounding of earnings (and dividends). This is even without dividend re-investment, as Buffett generally doesn’t reinvest the dividends back in the same company, but prefers to use them to purchase other undervalued stocks.

Charlie Munger and Warren Buffett are two living legends of our time. We are fortunate to learn from these investing stalwarts. These days, I learn more from Charlie Munger who is the catalyst behind much of Buffett’s investment success. I will end this post with one of my favorite quotes from him:

“It is remarkable how much long-term advantage people like us have gotten by trying to be consistently not stupid, instead of trying to be very intelligent.” Charlie Munger

Charlie Munger’s 1994 Harvard speech:

Raman Venkatesh is the founder of Ten Factorial Rocks. Raman is a ‘Gen X’ corporate executive in his mid 40’s. In addition to having a Ph.D. in engineering, he has worked in almost all continents of the world. Ten Factorial Rocks (TFR) was created to chronicle his journey towards retirement while sharing his views on the absurdities and pitfalls along the way. The name was taken from the mathematical function 10! (ten factorial) which is equal to 10 x 9 x 8 x 7 x 6 x 5 x 4 x 3 x 2 x 1 = 3,628,800.

5 comments on “Learning From The Investment Oracle (not the one you think)”