Loss aversion defines much of human behavior. We are so worried about the prospect of loss, that many studies show that finding $100 doesn’t give the same joy to offset the pain of losing $100. Some say, it takes as much as gaining $200 to offset the loss of $100. In other words, a loss feels twice as painful than a gain of same amount. Unfortunately, those quick odds aren’t available in real life investing or even in Las Vegas casinos.

Loss aversion defines much of human behavior. We are so worried about the prospect of loss, that many studies show that finding $100 doesn’t give the same joy to offset the pain of losing $100. Some say, it takes as much as gaining $200 to offset the loss of $100. In other words, a loss feels twice as painful than a gain of same amount. Unfortunately, those quick odds aren’t available in real life investing or even in Las Vegas casinos.

On one hand is a thrill of finally reaching financial independence or early retirement (FIRE). A long cherished goal for many aspirants. The 4% rule is a widely used standard to mark this accomplishment or if you wish to read up and become very conservative, you could use 3.27%, but who’s quibbling? 😊

On the other hand is a real worry you may outlive your portfolio. The media fuels this fear constantly. It’s hard to remain unaffected.

Understanding and managing risk is a key skill, as we saw in this article. That article also explained the difference between risk tolerance and risk affordability. Despite all the logical arguments, when real money is at stake, our rational brain can be overpowered by our emotional brain.

Queen Padme Amidala would say “May The Force Guide Your Amygdala”.

Our emotions are controlled by the Amygdala. No, it’s not the queen from Star Wars, as a kid once asked me. Amygdala is part of the limbic system that deeply stores all memories relating to emotions, and evokes them at different times and situations making us – as some might say – human. Being emotional is not always bad – it is a key requirement for compassion and empathy. Charity, helping out others and a big heart, in general, would not exist if not for emotions. Also, emotions can drive courage and doing the right thing. These are the “good” sides of the mighty Amygdala.

The “bad” sides of Amygdala come into play if the emotions make you nervous beyond reason, angry beyond sensibility, hateful without real cause and fearful without logic. It is these bad sides that hurt you as an investor, and hurt your chances of remaining happily FIRE’d.

I am not immune to the sneaky attacks by the Amygdala. I don’t have any more special weapons than you to dispel the mighty brain chemicals that it triggers to make me fearful, greedy or angry at times. I am learning to recognize its attack more these days.

So, what should we do then? We have a choice. Psychologists say that the only logical way to address your fears is to face them. To put this to use for the purpose of this article, we should stress test our portfolio and see how you react long before the event actually comes.

You can do the stress test in two ways, depending on whether you are an index investor or a dividend growth investor. For a detailed analysis between these two valid investing approaches, please see here.

Stress Test

Index Investors (example):

- Take your stock index portfolio and subtract 40% from it. First, take out your calculator. Multiply your investment portfolio’s current value by 0.6. (If you have current portfolio of $1 million x 0.6 = $600,000)

- Print the result in 36 point font (or even bigger) on your home or office printer. ($600,000 – yeah, this is what 36 pt Font looks like)

- Paste this number where you can see it every day for at least a week. Get used to seeing this reduced number. Close your eyes and imagine what would you feel if this number actually showed up on your screen after logging in today instead of what you had yesterday. Breathe deeply…let the moment pass.

- Take your expected living expenses and cut by 20%. Almost every one should have a 20% “fat” to trim in their expense budget during lean times. This is why I don’t believe in extremely frugal budgets (“lean FIRE”) because there isn’t any fat to cut. (Portfolio withdrawal of $35,000 in normal times, cut by 20% = $28,000)

- Take the percentage ratio of the slimmed down withdrawal and your shrunk portfolio value. If it is at or under 5%, BREATHE EASY! You have passed the test. ($28,000/$600,000 = 4.67%)

Even if you didn’t pass the test, don’t worry. Your retirement is not gloomy. It tells you something valuable about your retirement preparedness and what you need to do to hone up your skills to generate some side income or have a cash buffer to tide over lean times.

Dividend Investors:

The stress test for dividend investors is a bit more complicated but it is absolutely worth doing it. Here we go:

But worth it…

- Take your dividend stock portfolio and calculate the forward annual dividend income based on latest available dividend per share data from each company. (A portfolio dividend yield of 3.5% on a $1 million portfolio = $35,000 in dividends, based on current div/share data).

- Look back to 2008-09 Great Recession and analyze the dividend cuts for each of your holdings. Historical data is available in many dividend sites, Nasdaq, Google and Yahoo finance. I use Guru Focus. If your holdings did not pay dividends back then, assume the worse case dividend cut of a similar holding in the same industry. If some of your holdings (especially defensive sectors like utilities and staples) increased dividends during the recession, record that too. That pattern repeats often. In some cases, a stock may not have cut its dividend in the year the broader market entered a recession, but perhaps a year or two later (due to lag effect of recession in some industries). In that case, you have to look at the dividend data well past the recession end to check if there has been a cut. In my case, couple of my holdings delivered a cut in 2010, while keeping their dividends constant in 2008-09.

- Using the information in Step no. 2 above, recast your dividend portfolio and do a weighted average dividend reduction estimate across all your holdings. There is a very useful function in Excel and Google Sheets called “SUMPRODUCT” that allows you to calculate this in a jiffy across all your holdings. The hard part in this exercise is Step 2, collecting accurate historical data on dividends and adjusting for industry equivalents and splits, if any.

- The output from the previous step shows the actual (back-tested) impact on your dividend income during the most recent example of Great Recession.

As a dividend investor, what’s important is not what the aggregate index fund did, though it gives a benchmark. What’s critical for you is how your own current portfolio would have caused an income reduction during the Great Recession. In my own case, when I did this painful (but totally worthwhile) exercise following the above steps on my 40-stock portfolio, I came up with a figure of -8.5%.

We know that the next recession may not be like the previous one but the past data is all we have to go by. Our fear should be real – I mean, tied to a worse case scenario that’s already occurred rather than about an imagined apocalypse, which only feeds paranoia. That’s why past recessions are an excellent historical guide for us to study.

If you are worried this may not be ‘severe enough’ (Amygdala in action again), consider that the 2008-09 dividend cuts in S&P 500 companies was the second worst in the last 100 years, the worst being the Great Depression of 1930’s. Severe enough?

So, my current portfolio would’ve suffered a dividend income loss of 8.5% during the 2008-09 recession. Sure, some holdings cut 50% or even two-thirds of their dividends, but this was offset by many others that did not reduce their dividends and stayed at the same level in 2009 and 2010. Partially offsetting the big dividend cutters were some (like McDonald’s and utilities like Southern Company) that actually increased their dividend – it’s almost as if the recession never happened for them.

The overall impact was an income cut of under 10%.

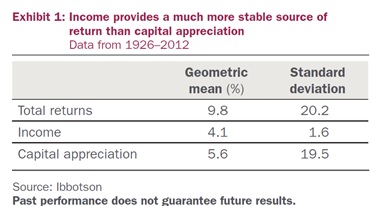

The portfolio, on the other hand, would have taken a much bigger hit during the recession than the cut in dividends. This is consistent with the 86-year Ibbotson study confirming the stability of dividends over capital gains. See the table below – note the massive difference in the standard deviation (volatility) between ‘income’ and ‘capital appreciation’. Higher the standard deviation, wilder are the swings in values. A standard deviation of zero means no change at all.

Dividends are stable, capital gains are fickle.

My own little back-test is consistent with the findings of the Ibbotson study.

If your living expenses can be cut by 20% during the recessionary years, then a dividend cut of 8.5%, or even 15-20% would prevent you from selling any shares at the bottom of the bear market.

Being forced to sell shares at the bottom to fund living expenses is precisely what causes retirement failure. If you sell too much at the bottom, then you won’t have enough invested to benefit from the bull market that eventually follows a bear market. This is the basis of all safe withdrawal rate studies.

Selling shares at the bottom is a root cause of what the investing world worries about – sequence of return risk (SRR). A shout-out to Big ERN here for his excellent series of articles on safe withdrawal rates, especially on SRR, which is critical to all retirees.

Fear, at its core, is a fundamental human emotion. It cannot be avoided, but it can be managed and controlled with data. Have you stress-tested your portfolio? What do you think of the above methods? I would also be curious to know how people with investment real estate stress test their portfolios. Please share your thoughts below.

Raman Venkatesh is the founder of Ten Factorial Rocks. Raman is a ‘Gen X’ corporate executive in his mid 40’s. In addition to having a Ph.D. in engineering, he has worked in almost all continents of the world. Ten Factorial Rocks (TFR) was created to chronicle his journey towards retirement while sharing his views on the absurdities and pitfalls along the way. The name was taken from the mathematical function 10! (ten factorial) which is equal to 10 x 9 x 8 x 7 x 6 x 5 x 4 x 3 x 2 x 1 = 3,628,800.

13 comments on “Stress-test Your Financial Independence”